Summary:

On 13 March 2018, the EU Member States reached a political agreement on the tax intermediaries’ directive (“the Directive”). The Directive was formally adopted by the EU Council as amendment to Council Directive 2011/16/EU on administrative cooperation in the field on taxation. The Directive, commonly known as “DAC6”, provides for the mandatory automatic exchange of information in the field of taxation with respect to reportable cross-border arrangements.

The Directive reflects the objectives of Action 12 of the BEPS Action Plan and is designed to enhance transparency to prevent aggressive cross-border tax planning.

DAC6 was implemented into Cyprus Law on 31 December 2019.

Due to COVID 19, the Cyprus Tax Authorities published on 22/05/2020, the proposal of the EU regarding the grant of extension on deadlines for reporting under the Directive 2011/16/EU Directive on Administrative Cooperation (DAC), in view of the Covid-19 outbreak and the disruption caused in the business sector at global level (see below).

Key Features of the Directive:

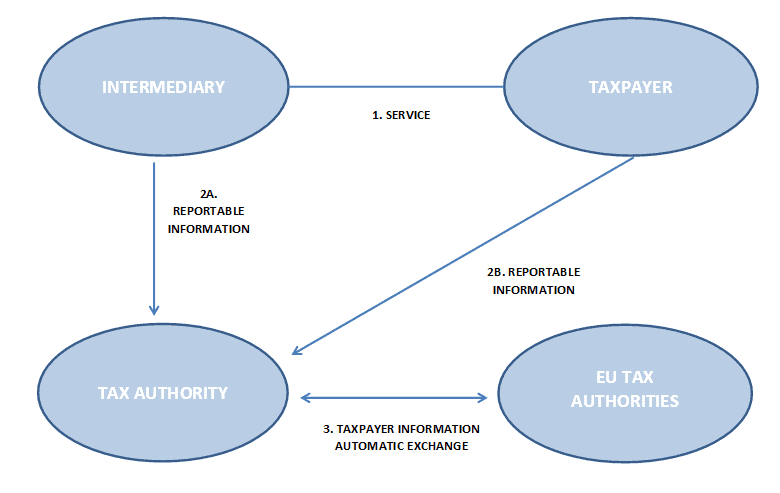

Under the Directive, intermediaries have the primary obligation to report arrangements to the tax authorities in the country in which they are resident. The latter will then automatically share the information with the Tax Authorities of all other member states on a quarterly basis. The Directive gives Member States the option to exempt intermediaries from the obligation to report where the reporting obligation would breach legal professional privilege (LPP). If there are no intermediaries who can report, the obligation will shift to the taxpayers.

What is a Reportable Cross- Border Arrangement (RCBA):

A RCBA refers to an arrangement or a series of arrangements concerning either more than one member state, or a member state and a third country.

Intermediaries:

Under DAC6, “intermediaries” are subject to reporting. An intermediary is any person who:

- designs, markets, organizes or makes available for implementation or manages the implementation of RCBA

- provides, directly or by means of other persons, aid, assistance or advice with respect to designing , marketing, organizing, making available for implementation or managing the implementation of RCBA

Such persons may include tax advisors, accountants, auditors, banks, lawyers, administrative services providers, or any other professionals who undertake any of the above acts.

In certain situations, the obligation to report can fall on the taxpayer itself, such as where an intermediary is a Non-EU person, where no intermediary is involved, or where an intermediary does not disclose owing to legal professional privilege.

Reportable Arrangements:

Under the Directive, an arrangement is reportable if:

• The arrangement meets the definition of a cross-border arrangement; and

• The arrangement meets at least one of the hallmarks A-E (see below) of the Directive.

The hallmarks can be distinguished as hallmarks which are subject to the main benefit test (MBT), and those which by themselves trigger a reporting obligation without being subject to the MBT

Hallmarks and Main benefit test (MBT):

In accordance with DAC6, under the Bill, the MBT will be satisfied if it can be established that “the main benefit or one of the main benefits which, having regard to all relevant facts and circumstances, a person may reasonably expect to derive from an arrangement, the obtaining of a tax advantage.”

Hallmarks are categorised from A to E as follows:

- Hallmark category “A”: arrangements whose tax benefits are subject to confidentiality arrangements, that give rise to performance fees or mass marketed schemes;

- Hallmark category “B”: arrangements such as the contrived acquisition of loss-making companies, the conversion of income into capital or other forms of income, or so-called circular transactions;

- Hallmark category “C”: arrangements that give rise to tax deductions without a corresponding amount of taxable income, to certain double reliefs or deductions, or other mismatches;

- Hallmark category “D”: arrangements that have the effect of undermining the CRS or the rules on identification of beneficial ownership;

- Hallmark category “E”: arrangements concerning transfer pricing.

Reporting and exchange of information:

Tax intermediaries will have to report arrangements that fall within the scope of the directive within 30 days after the arrangement is made available for implementation/ready for implementation or the first step in the implementation has taken place (although in certain situations, the intermediary will be required to submit a report every three months). Where an intermediary (or taxpayer) is required to submit information on covered arrangements with the competent authorities of more than one member state, the information must be filed with one member state according to a specified hierarchy.

Scope of taxes covered:

The Directive covers arrangements involving all types of direct tax, including corporate, personal, capital gains and inheritance tax.

Reportable Arrangements:

Information on the arrangement would include:

- Identification of all taxpayers and intermediaries involved, including

- Tax residence.

- Name, date and place of birth (if an individual).

- Tax Identification Number (TIN).

- Where appropriate, the associated persons of the relevant taxpayer.

- Details of the relevant applicable hallmark(s).

- A summary of the arrangement, including (in abstract terms) a summary of relevant business activities.

- The date on which the first step in implementation was or will be made.

- Details of the relevant national law.

- The value of the cross-border reportable arrangement.

- Identification of relevant taxpayers or any other person in any Member State likely to be affected by the arrangement.

Penalties:

Where an intermediary or relevant taxpayer fails to report an arrangement to the Cypriot tax authorities, an administrative fine between €10,000 and €20,000 is expected to apply.

COVID 19 – Extension period

Based on the new EU Directive, each EU Member State is allowed on an optional basis to postpone DAC6 deadlines as follows:

- For filing reportable cross-border arrangements (RCBAs) the first step of which was implemented between 25 June 2018 and 30 June 2020, the filing deadline has been extended to 28 February 2021

- For filing RCBAs where the triggering event for the reporting took place between 1 July 2020 and 31 December 2020, the period of 30 days for filing information shall begin on 1 January 2021

- For filing marketable RCBAs the first periodic report shall be made by the intermediary by 30 April 2021

- The first automatic exchange of information between EU Member States, may be delayed but shall take place no later than 30 April 2021

The new EU Directive additionally provides for the possibility to postpone the deadlines by another 3 months in case EU Member States have to implement lockdown measures.

Comments:

Taxpayers and intermediaries involved in cross-border arrangements should asses their transactions and procedures for recording and reporting tax arrangements in order to be fully prepared for meeting these obligations.