Cyprus Holding Company

Cyprus, as a well established International Financial Centre, has always been an excellent location for holding companies from tax and business perspective, among others. Cyprus holding company is an important consideration in any international structure where there is a desire to minimize the tax imposed on income and gains.For professional advice and assistance please contact solutions@oxfordcy.com.

A Cyprus holding company is a limited liability Company that has the purpose of holding shares in other companies. In essence, holding companies are set up as an effective means of consolidating ownership of operating subsidiaries. When deciding on a jurisdiction of a holding company, both tax and non- tax factors must be carefully taken into consideration.

CYPRUS HOLDING COMPANY KEY BENEFITS

- Cyprus has the lowest corporate tax rate in Europe at 15%;

- There is an exemption from tax on dividends when they are received from overseas. The exemption will not apply if i) the foreign company paying the dividend receives, directly or indirectly, more than 50% of its income from investment activities. ii) the foreign company tax rate due is substantially lower than the corresponding tax burden in Cyprus, as determined under the applicable provisions of the Cyprus Income Tax Law.;

- Exemption from withholding tax on payment of Dividends, Interest and Royalties;

- Cyprus is an attractive location for the establishment of an IP holding and development company, offering an efficient tax rate (effective corporate tax rate as low as 3%) as well as the legal protection afforded by EU Member States and by the signatories of all major IP treaties and protocols;

- Profits arising from the disposal of qualifying securities are generally exempt from Cyprus income tax. Capital Gains Tax (CGT) is imposed at the rate of 20% on gains arising from the disposal of immovable property situated in Cyprus and on the disposal of shares in companies that directly or indirectly derive their value from such property, subject to the applicable provisions, exemptions and reliefs under the Capital Gains Tax Law;

- Cyprus has entered a beneficial network of double tax treaties and is in negotiation with many more countries. These treaties have the advantage of lowering or eliminating the withholding tax on dividends, interest or royalties at source;

- As a full member of the European Union, Cyprus offers the benefits from the provisions of the EU directives;

- Re-organisations: Reorganisations: Profits or gains arising as a result of a qualifying reorganisation are exempt from Cyprus corporation tax, capital gains tax and transfer fees.A qualifying reorganisation includes, inter alia, mergers, divisions, transfers of assets and exchanges of shares involving companies that are tax resident in Cyprus and/or companies that are not tax resident in Cyprus, provided the relevant conditions of the Cyprus tax legislation are satisfied;

- Cyprus does not impose statutory debt-to-equity (thin capitalisation) rules. However, the deductibility of borrowing costs is subject to the Interest Limitation Rule implemented under the EU Anti-Tax Avoidance Directive (ATAD), together with the applicable transfer pricing and arm's-length principles.

TAX LOSSES

- Tax losses may be carried forward for a period of five years and may be offset against future taxable profits, subject to the provisions of the Cyprus Income Tax Law;

- Losses incurred by a foreign permanent establishment (PE) of a Cyprus tax resident company may be offset against the taxable profits of the Cyprus company. Where such losses have been utilised, any subsequent profits of the foreign permanent establishment become taxable in Cyprus up to the amount of the losses previously claimed (loss recapture), subject to the applicable provisions of the Cyprus Income Tax Law.

GROUP LOSSES RELIEF

- Tax losses of one Cyprus tax resident group company may be surrendered and offset against the taxable profits of another Cyprus tax resident group company, provided the companies are members of the same group for the relevant tax year and the conditions for group relief under the Cyprus Income Tax Law are satisfied;

- Group relief is available where one company is the 75% direct or indirect subsidiary of another company, or where both companies are 75% direct or indirect subsidiaries of a common parent company, provided that the conditions for group relief under the Cyprus Income Tax Law are satisfied;

- Losses brought forward will not be available for group relief, only the current year losses can be transferred.

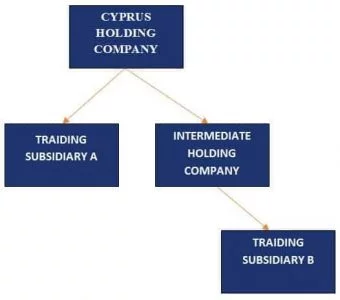

CYPRUS HOLDING COMPANY DIAGRAM

- Dividends received by a Cyprus holding company are generally exempt from Cyprus corporate income tax under the Cyprus participation exemption regime, subject to the applicable conditions.

- Subsidiaries may be established in Cyprus, the EU or any other jurisdiction.

- Where the conditions of the EU Parent-Subsidiary Directive are met, dividends paid by an EU subsidiary to a Cyprus parent company may be exempt from withholding tax.

- Where a subsidiary is resident outside the EU, relief from withholding taxes may be available under the applicable Double Tax Treaty.

- Where an intermediate holding company is established in another jurisdiction, the group may also benefit from that jurisdiction’s treaty network, subject to the applicable domestic laws, treaty provisions and anti-abuse rules.

SO WHO CAN BENEFIT?

- EU residents who have holding companies outside the EU

- EU residents with subsidiaries outside the EU if can employ the Double Tax Treaties.

- Non-EU residents with subsidiaries in the EU.

- Non EU residents with subsidiaries outside the EU utilising the Double Tax Treaties of Cyprus or the Intermediate Holding Company.