Cyprus Alternative investment fund (AIF) and Registered Alternative Investment Fund (RAIF):

Cyprus AIF Regime: In July 2018 the Republic of Cyprus replaced the original Alternative Investment Fund (AIF) Law of 2014 and introduced a more modern and improved regime for AIFs.

Following the changes in law, Cyprus is now fully aligned with the EU Directives which includes the Alternative Investment Funds Manager Directive. This allows for any AIF that is established in Cyprus to be sold on a private placement basis or to professional investors through the EU.

The new law allows more investment structuring possibilities, supervision of Cyprus AIFs, upgraded rules on authorisation and regulations on responsibilities of directors and managers.

An Alternative Investment Fund (AIF) is an investment that is undertaken by a number of investors with aim to raise external capital and invest it, following a clear investment policy, in order to benefit them.

AIFs are all investments that are not covered in the European Directive on Undertakings for Collective Investment in Transferable Securities (UCITS). An AIF is an investment of non-traditional assets. For example it can be a hedge fund, a private equity, a real estate etc.

Setting up the fund:

A business is normally directed via a fund when an investor does not desire to be involved in the day to day running of their investment however still seeks a profitable return.

Investor categories:

Capital for an AIF can be raised from professionals or well-informed investors. See analysis below:

Professional investor:

In order for an individual to be considered a professional investor, they must meet at least two of the below criteria:

- During the last four quarters, this investor must have executed at least 10 transactions of similar size per quarter;

- The investor’s portfolio must exceed either in cash or in other financial instruments the amount of €500,000;

- The investor must have worked for at least one year in the professional position and have the appropriate expertise and experience

Well-informed Investor:

A well informed investor is an individual that invests at least €125,000 in the fund or has been evaluated and classified as a well-informed investor by a licensed bank/credit institution, an authorised investment firm or an authorised management company. The investor must have proper knowledge and must also confirm in writing that he is aware of all the relevant risks of the investment.

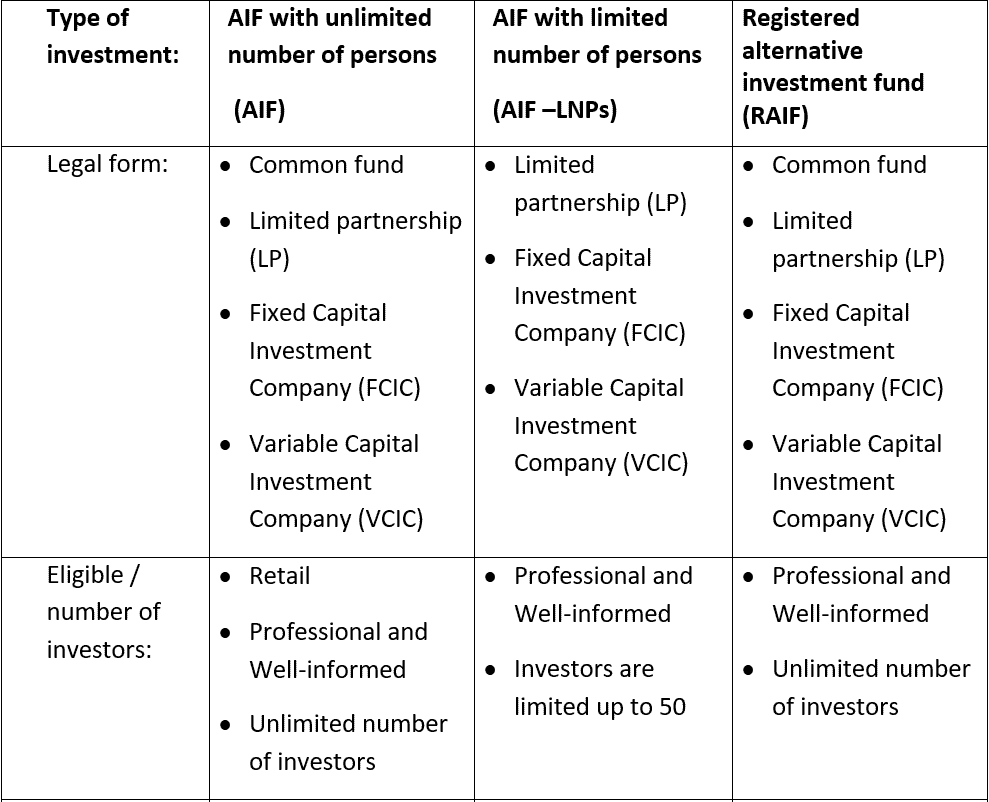

Legal Forms:

An AIF can be set-up in one of the below legal forms:

- Common Funds: The fund is structured as a contract between investors and is manager by an external manager. Each partner is accountable up to the amount of the payment they made to the fund

- Limited Partnership (LP): This form of fund allows high flexibility in regards to the rights of the partners

- Fixed Capital Investment Company (FCIC): A limited liability company with a fixed capital

- Variable Capital Investment Company (VCIC): A limited liability company with a variable capital

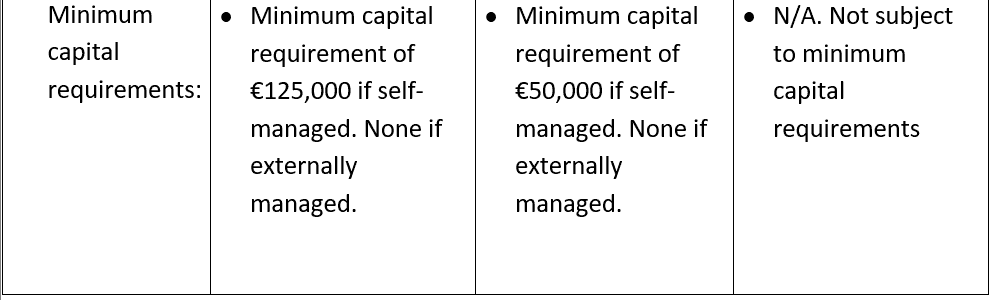

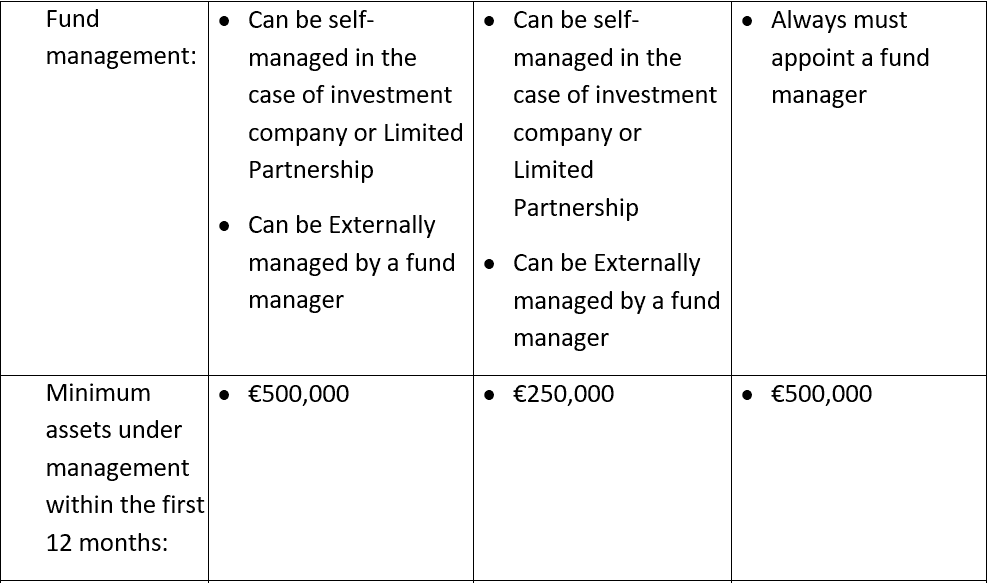

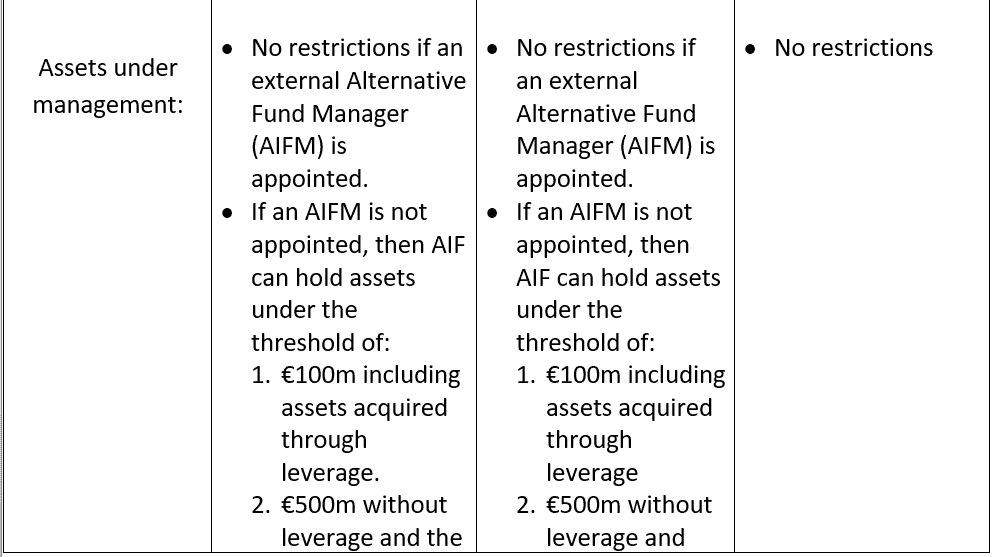

Types of Cyprus AIFs:

The below table is a summary of three options of Cyprus AIFs and its characteristics;

- An AIF with Unlimited number of persons (AIF)

- An AIF with Limited number of persons (AIFLNP)

- A Registered AIF (RAIF)

Advantages of setting up an AIF in Cyprus:

- Units of AIFs can now be listed on a number of stock exchanges and are freely transferable

- Registered AIFs do not require to be licenced. Registered AIFs merely need to be registered on the regulator’s register. This can be done in a period of 30 days after submission

- Cyprus has no restrictions in regards to the type of investments, therefore there is the opportunity to form AIFs with unlimited investment compartments – Umbrella funds

- Low set-up and maintenance charges

- A Cyprus AIF can be self-managed by its Board of Directors, always subject to the approval of CySEC (Cyprus Securities and Exchange Commission)

- Cyprus AIFs can benefit from Cyprus favourable tax system – See analysis below of how Cyprus AIFs are taxed

AIF/RAIF offers the following incentives:

- Collective Investment: A single investor is not burdened with the full amount that would be required for the purchase of assets, if he was acting on his own.

- Diversification: Investors become the owners of units in the AIF/RAIF. The AIF/RAIF pools the money invested by many Investors and uses this large mass to buy several assets so that concentration risk is limited.

- Protection: All the activities required to manage assets are performed by the professionals responsible for the AIF/RAIF (administrator, auditor). What is more, the funds are regulated by a competent authority and property management is performed by licensed professionals (oversee construction, manage tenants, perform maintenance, pay taxes etc.).

- Transparency: Investors will be updated for the value of investments and the policies of the AIF/RAIF through the periodic reports that are prepared and circulated to them based on regulatory requirements.

Key Features of a RAIF:

- No licensing required – RAIFs do not need to be licensed/authorised by CySEC and thus they do not fall under the direct supervision of CySEC. However, the establishment of a RAIF will need to be notified to CySEC and be included in a CySEC RAIFs register.

- RAIFs will be supervised by a licensed Alternative Investment Fund Manager (“AIFM”), which supervises the RAIF and provides certain mandatory services (risk management, compliance, internal compliance audit etc.).

- No initial capital requirements – There are no minimum initial capital requirements for a RAIF, but minimum assets under management of at least EUR 500,000 or currency equivalent to be reached within the first 12 months of receiving authorization (may be extended to 24 months).

- No investment restrictions – There are no investment restrictions for a RAIF, with the exception that RAIFs cannot set up as Fund of Funds, Money Market Funds or Loan Origination Funds.

- A RAIF can take all available legal forms and is allowed to invest in non-financial assets.

- Unlimited number of Investors – A RAIF has no maximum number of investors.

May only be addressed to Professional/Well-informed investors.

- Possibility for creation of multiple compartments– RAIFs may be set up as umbrella funds which have separate compartments treated as a separate legal entity. Thus, there is an option for umbrella structure with multiple investment compartments (‘sub-funds’), provided that this is mentioned in the RAIF’s regulatory documents.

- Units of RAIFs may be listed.

- Requirement to appoint local Depositary.

- “Pass-porting” rights for fund distribution within the EU Appointment of local depository.

Taxation of AIFs RAIFs in Cyprus:

- The Cyprus tax system exempts all profits made from the disposal of securities.

- No tax is imposed on dividend income and capital gains of Cyprus tax resident fund (subject to conditions)

- No withholding tax on dividend distributions, interest and royalties to non-residents

- Corporation tax of 12.5% which is amongst the lowest rates in the EU

- No stamp duty on issue of units of AIFs/RAIFs

- Services provided by the Investment Management and Fund Administrators are not subject to any VAT

During the last few years Cyprus has seen a growth in the funds industry and especially now that it fully aligns with the EU regulations. For more information and advice in regards to setting up a fund in Cyprus and how this can benefit you, please contact us.