Cyprus Holding Company

Cyprus, as a well established International Financial Centre, has always been an excellent location for holding companies from tax and business perspective, among others. Cyprus holding company is an important consideration in any international structure where there is a desire to minimize the tax imposed on income and gains.For professional advice and assistance please contact solutions@oxfordcy.com.

A Cyprus holding company is a limited liability Company that has the purpose of holding shares in other companies. In essence, holding companies are set up as an effective means of consolidating ownership of operating subsidiaries. When deciding on a jurisdiction of a holding company, both tax and non- tax factors must be carefully taken into consideration.

CYPRUS HOLDING COMPANY KEY BENEFITS

- Cyprus has the lowest corporate tax rate in Europe at 12.5%;

- There is an exemption from tax on dividends when they are received from overseas. The exemption will not apply if i) the foreign company paying the dividend receives, directly or indirectly, more than 50% of its income from investment activities. ii) the foreign company tax rate due is substantially lower (meaning less than 5%) than the Cyprus rate;

- Exemption from withholding tax on payment of Dividends, Interest and Royalties;

- Cyprus is an attractive location for the establishment of an IP holding and development company, offering an efficient tax rate (effective corporate tax rate as low as 2.5%) as well as the legal protection afforded by EU Member States and by the signatories of all major IP treaties and protocols;

- Profit from dealing of securities is not subject to tax. Capital Gains tax of 20% is only imposed on the sale of immovable property situated in Cyprus or of shares of unlisted companies that own such property in Cyprus, subject to certain exemptions and reliefs. There is no Capital gains tax for the sale of immovable asset in Cyprus;

- Cyprus has entered a beneficial network of double tax treaties and is in negotiation with many more countries. These treaties have the advantage of lowering or eliminating the withholding tax on dividends, interest or royalties at source;

- As a full member of the European Union, Cyprus offers the benefits from the provisions of the EU directives;

- Re-organisations: When profits and/or gains are developed by re-organisation reasons (which means a merger, division, transfer of assets and exchange of shares that involve companies which are resident in Cyprus and/or non-resident in Cyprus) they are exempt from corporation tax, capital gains tax and transfer fees;

- No debt-equity restrictions, no substance requirements, no minimum holdings period and no thin cap rules apply to deduction of interest.

TAX LOSSES

- The tax losses from the year 1997 can be carried forward indefinitely and can be used against future profits;

- Any losses incurred abroad by a permanent establishment of the Cyprus Company they can also be offset against profits of the Cyprus Company.

GROUP LOSSES RELIEF

- Losses of one company in the group can be set-off against the profits of another company if the companies are tax resident in Cyprus and if they belong to the same group for the whole year appraisal;

- Group relief applies when the holding company owns at least 75% of the share capital of the subsidiary or among companies which belong to the same group for the whole year with 75% each directly or indirect in the other company;

- Losses brought forward will not be available for group relief, only the current year losses can be transferred.

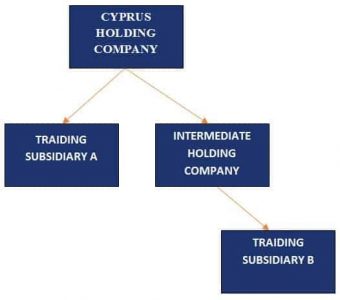

CYPRUS HOLDING COMPANY DIAGRAM

Diagram showing the use of a holding company with direct and indirect holding in trading companies.

- Dividend received is exempt from taxation if the holding company holds shares directly in trading company A or Intermediate Holding Company.

- Subsidiaries can be resident anywhere

- If subsidiary A is EU resident then no withholding tax from paying subsidiary based on EU Parent – Subsidiary directive.

- If Subsidiary A is outside the EU then Cyprus Double Tax treaties are implemented.

- The group can also take advantage of the Double Tax Treaties of the non-Cypriot Intermediate Holding Company.

SO WHO CAN BENEFIT?

- EU residents who have holding companies outside the EU

- EU residents with subsidiaries outside the EU if can employ the Double Tax Treaties.

- Non-EU residents with subsidiaries in the EU.

- Non EU residents with subsidiaries outside the EU utilising the Double Tax Treaties of Cyprus or the Intermediate Holding Company.

Cyprus Company

- Cyprus Company Formation

- Cyprus Investment Firm (CIF) Licence

- Cyprus Shelf Companies

- Cyprus Holding Company

- Cyprus Intellectual Property (IP) Company

- Cyprus Tax Residence

- Cyprus Bank Account

- Cyprus AIFs

- Cyprus RAIFs

- Cyprus Company Redomiciliation

- Cyprus International Trust

- Cyprus Serviced Offices

- Headquartering